Feel free to write us

a message.

A New Trading System Test

event_note 13.08.2019

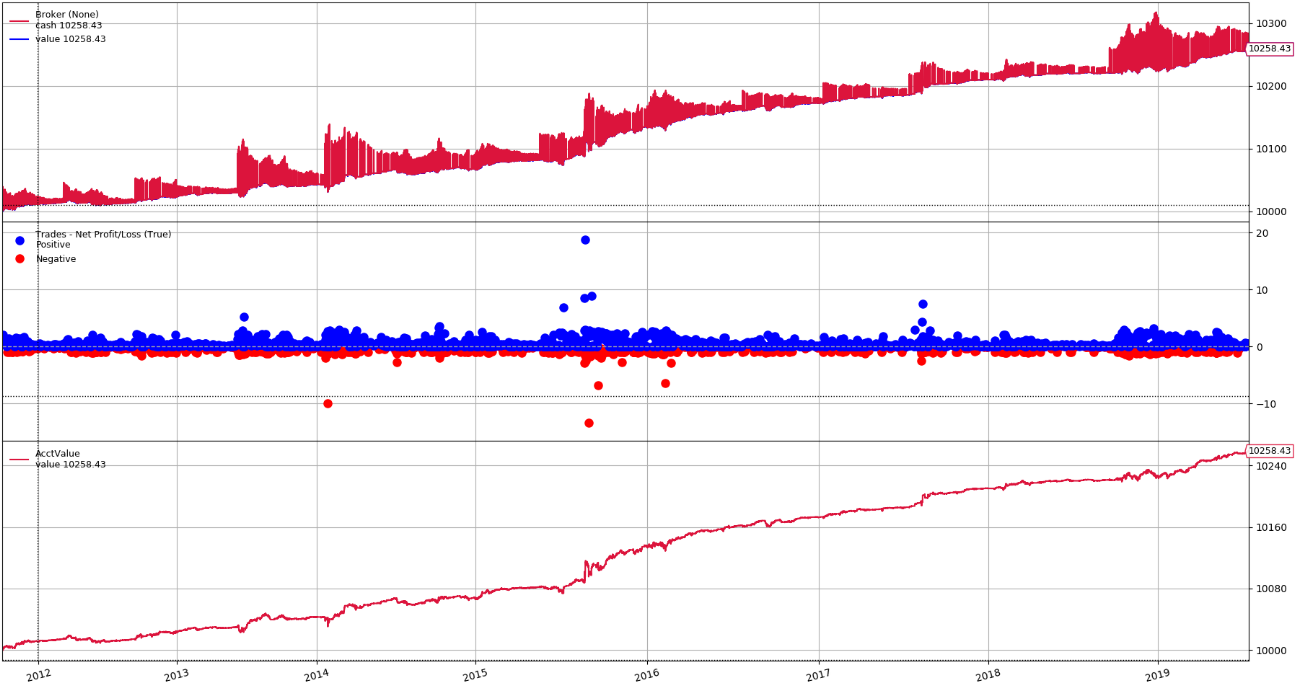

Our R&D team developing tools for asset optimization and management, cooperating with Mendel University in Brno has launched a new trading system based on long-term effects of contango decay and volatility lowering. The system composes synthetic short position via option contracts for underlying asset ETF UVXY. An alfa factor is formed with regular technical indicators calculated from five-minute bars.

The most difficult task in backtesting script development was to manage situation where the script takes values based on five-minute bars calculation but the trading trigger may occur at anytime (not at time five-minute bar closes only). The solution depends on dynamic bar creation which gradually collects the last bar data (every minute). The scripts looks at this bar as five-minute bar.

After the firts test, we made (consistent with our principles) optimization via parameter sweep. The fitting rapidly improved the performance and stability of the system (out-of-sample). Due to esotheric assets utilitization (as the options are) we proceed to the next step of our test – the paper trading. We have chosen the paper trading rather early because of option strategies difficulties. We have to face missing option data with interpolation and extrapolation of volatility surface with appropriate model. Simply said we will calculate the missing data but it is slightly time demanding.

All in all the next trading system was launched besides Momentum Formula, indeed temporary for testing regime only. Launch more than one trading system provide us valuable information for portfolio optimization.

We are going to report the performance and next development of the system through next posts.

Michal Dufek, Head of Financial Research Software Development